My average monthly savings of my disposable income (after bills) since October 2019 is 83.71%. Yes, you read that correctly, 83.71%. My 5 months prior to COVID-19 average savings are 82.30%. Admittedly this is slightly lower as expected due to lockdown but these savings are still huge. In absolute terms, I spend on average just over £200 a month after monthly bills as a young adult whereas this used to be around £400. In 11 short steps I am going to talk you through exactly how to control spending.

If you want to skip straight to the best method incorporating all the below and my secret, click here.

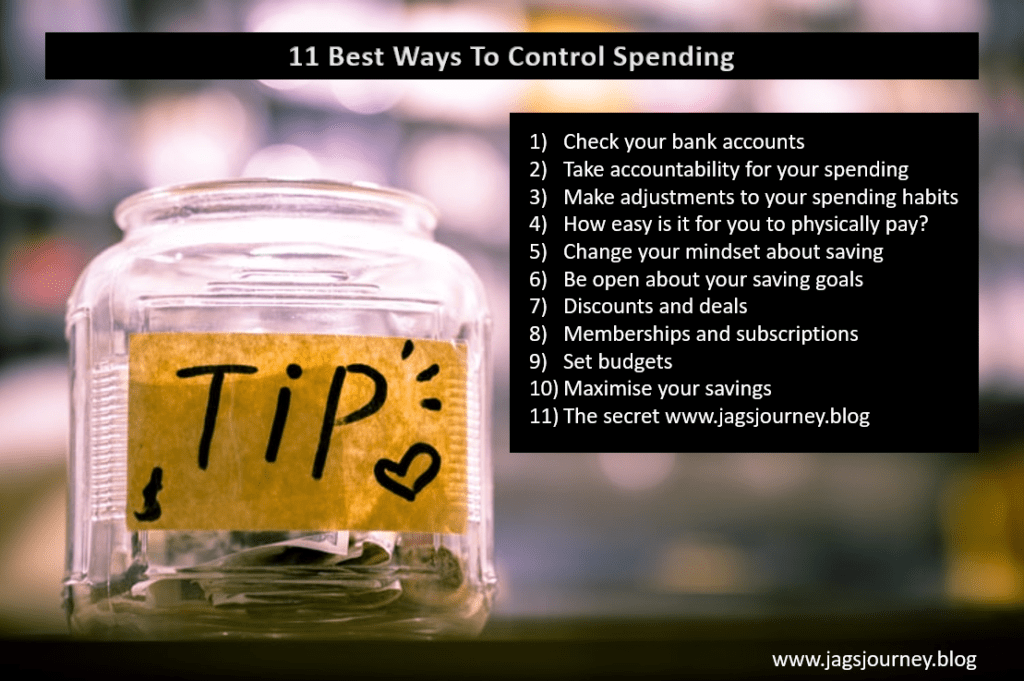

Table of Contents

- 1) Check your bank accounts

- 2) Take accountability for your spending

- 3) Make adjustments to your spending habits

- 4) How easy is it for you to physically pay?

- 5) Change your mindset about saving and spending control

- 6) Be open about your saving goals and spending control

- 7) Discounts and deals

- 8) Memberships and subscriptions

- 9) Set budgets to control spending

- 10) Maximise your savings

- 11) The secret behind my spending control

1) Check your bank accounts

It sounds very obvious but actually check your bank accounts and how much you have available to spend. Do not just trust you have been paid each month or leave it to someone else such as your partner. If you want to control spending and save, you need to actually take control.

I have heard countless times “I’m too scared to check my accounts tomorrow”. I have been guilty of saying these words after a night out and I know a lot of people can relate to this. However, this attitude to spending will not maximise your savings. You need to know the damage so you can act accordingly to damage control.

I was quite against getting bank account apps initially. With my job I am working on my laptop daily so it was easy for me to check without getting the apps. However, I finally gave in and have not looked back. It is very helpful having these to hand. The easier it is to check, the more likely you are to do it.

2) Take accountability for your spending

I cannot stress enough how important it is to take accountability for your spending. For me this is probably the most critical step to saving big. It is very easy to spend without thinking twice about where your money is going. I am now challenging you to think twice about your spending down to the penny. You need to be able to justify to yourself whether the takeaway was needed. Turning a blind eye to things like this will not help you control spending or save as these amounts all add up!

3) Make adjustments to your spending habits

I am not saying you cannot treat yourself anymore but you do need to realise that all those morning coffees add up. Prioritise what is important you to and recognise what spending is necessary. Separate your wants from your needs. You can buy those wants but in months where you will not have as many socials. You may be thinking what the point is if you are going to buy it in the end anyway. However, the point is training your mindset to save. Instead of buying a cup of coffee from Costa, buy a pack of their coffee beans and make it yourself.

I reckon most people would spend a lot of their extra money on eating out. Paying for sandwiches at lunch that could be made at home. A £3 meal deal five days a week is £15 but you probably could have got all the ingredients and made it yourself for £5. A nice £10 saving and demonstrating good spending control. You need to make the time for what is important.

Speaking of time, if you work reimburses you for expenses, stay on top of these and submit your expenses in a timely manner.

TOP TIP: This is a recent addition to this blog but a very good one. If you are ordering takeaway online, it is likely to be much cheaper ordering direct than through Uber Eats for example. You will be surprised how much extra is added to an item (around £1). If it is local, order directly by phoning up and collect instead. I have managed to save up to £13 through this! If you want it delivered then see if the takeaway offer their own delivery service. I will talk about discounts further down but do not be fooled by these promo codes. It still probably works out to be more expensive!

4) How easy is it for you to physically pay?

One thing I do not have is Apple Pay and I do not think I ever will get this. If you make it too easy to access and spend your money, you most likely will. If you are someone who will happily tap away at contactless payments, reassess your method of payment. Go that extra mile to get cash out and use this instead. You really do need to be conscious of spending and implement spending control.

If you are going somewhere and you do not need to spend money, do not take it. Take the emergency £10 with you or borrow from a friend at the time if you have to. If you are one to give in to spending on things you do not need, reduce the opportunity to do so.

Something that has worked for me is having two banks accounts. One I use for direct debits and the other is strictly for savings. This savings account is linked to my credit card (limit £1500) which I pay off with a direct debit each month. I am fortunate not to need a credit card but I have this to build my credit score.

The benefit of two accounts is that I can move money across to my savings account and this is now essentially out of bounds for spending. I do not have the card for this account to spend even if I wanted to. In the worst case I would transfer money back to the other but this would be disappointing and is avoided. This method allows me to split out my savings making it hard to dip into them.

5) Change your mindset about saving and spending control

I know what you may be thinking that this blog is basically about how to be ‘tight’. Wrong. This blog is helping you to become more aware of your spending and to take the reins. Being tight is not a bad thing, it just means you are serious about spending. You do not need to take this to extreme lengths to make good savings. You can still buy a round or two for your family/friends but factor this into your expectation for your monthly savings. Know that if you are going to be getting the rounds you may not be able to get as many takeaways that month.

If you are paranoid about being called tight, explain your saving goals. People will respect that you are trying to control spending. If you do not want to be the friend chasing up £1.49 debt, don’t do it. Instead knock it off the amount you owe later on.

6) Be open about your saving goals and spending control

As briefly mentioned above, be open about your savings goals and spending control. Talk to your close friends and family about it. Not only will you have yourself to answer to about your spending but knowing others will question your spending too.

This could also encourage those around you to do the same. You could even turn this into a little competition with your loved ones. Be the one who can save the most! I have actually done this and it weirdly became quite fun, especially since I won.

7) Discounts and deals

Before discounts, make sure you are shopping around and buying at the best available deal. Once found, really make the most of the discounts available to you. It is so easy to just check out and buy but you should take the time to sign up to the website to get the 15% off. If you hate getting the emails, unsubscribe straight after. One thing I do is spend at least a few minutes looking for discount codes online before buying anything. Granted there may not be any but at least try.

If you are an ACA student, did you know you are eligible to student discounts? You should if you read my blog about the ACA! Do not miss out on these opportunities. I have used Student Beans and it has saved me at least £100 this year. If your relatives are students, make the most of their discounts if they will be in your household using the same goods. Make the most of work perks, loyalty cards and free subscriptions. Credit cards also give cash back so select the company where you know you are going to spend.

I honestly do really maximise here where I can. I was given a free Costa gift card worth £5 from work last Christmas. This was not used within the year and it expired so I then emailed and called up to get this renewed rather than letting it go to waste. Recognise that every saving adds up. If it is your turn to order takeout but your friend has the discount available, use theirs but transfer the money.

Where I said about buying your wants in months with less spending, Black Friday is great for this. Be clever with your spending because it will pay off.

8) Memberships and subscriptions

On the point of subscriptions, if you sign up for a free subscription, make sure you cancel in time! Do not be the person who gets charged because you cancelled too late. Or even worse, the one who kept paying as they did not check their accounts to realise. Set a reminder in your calendar to cancel or better yet, you can cancel after signing up. This will still give you the free trial but will make sure you do not get charged. Additionally, if you have paid for one years subscription set that reminder to make sure your next annual payment is something you want to carry on with.

Memberships also need to be kept under control. For example, your gym membership. If you have not been going to the gym during COVID, did you freeze or cancel your membership? Again, these payments are adding up!

At the end of 2020 I got laser eye surgery which meant my monthly contact lens payments were no longer needed. In November 2020 I rang my lens provider and cancelled my direct debit. Shortly after I received a letter stating I had one month left to pay. I would rather this than pay for the next three months supply I will not need.

9) Set budgets to control spending

Like I said, it is not about being tight. Get your friends and family on board. If you are buying rounds, set a target budget in your head. If you are buying birthday presents, agree the budget. This also helps avoiding disappointment when you are the one who spent more in the end. Even give a range of ideas of things you actually need so you end up saving here too but can still feel surprised.

The whole idea is about training your mind. You need to plan for when you are going to spend more and when are you able to save. Mentally budgeting really does help. Know how much you want to save each month and work towards it. Achieving this goal will come with time and practice but this is something you can get better at.

10) Maximise your savings

You have read all the above and now know how to control your spending. It is mind over matter and really is quite simple in theory. If you have mastered the above, you are now ready to really think about if you are maximising your savings. If you are paying credit card interest monthly but have the funds available to pay this off and avoid interest, why are you doing this? Avoid the interest payments! If there is any way to turn this into an interest free payment, do it. Borrow money from a loved one if possible and make sure to pay them back instead.

In addition to this, are you using lifetime individual saving accounts (LISAs) or ISAs to save? This is similar to how I have a separate savings account so the money is not easily available to spend. However, these investments can give better returns and beat inflation.

I am very risk averse but a LISA is a great way to get up to £1,000 free each tax year. You need to budget to put in £4,000 aside in the year to achieve this but who does not love free money? The LISA can only be spent on a first home or for retirement. Either way, it is a great way to maximise your savings.

ISAs depending on what they are invested in can bear greater risk. I may be ACA exam qualified but this does not give me the qualification to give financial advice. My sister Jay is actually a financial adviser so if you have large sums of money sitting in a bank account depreciating, get in touch. I would also point you in Jay’s direction if you wanted a free financial review or general advice.

Trading: For anything trading, check out LogikFx – my knowledge is extremely limited here but LogikFx is the place to go!

11) The secret behind my spending control

You may be wondering how I was able to provide the initial statistic such as 83.71% monthly savings. It is definitely not made up and I have all the data behind it. The answer is my finance spreadsheet that I started in 2018. This spreadsheet is something I LIVE by. It really puts all the above into practice in terms of training your mindset and getting better at budgeting. This spreadsheet truly has made me accountable of all my spending. If you wanted to know how much I spent on taxis in December 2018, I can tell you (£34.79). In February 2019 my monthly savings were 63.13% of my disposable income. This goes to show how I have improved my mindset and developed my spending control.

There are apps that allow you to track your spending categories but I do not think this helps with accountability. When you have a spreadsheet to put these details into, you really do think twice and justify your spending. This may not work for everyone but if you are serious about saving, it is definitely a great place to start. I cannot imagine my spending life without this.

A full professional walkthrough of the spreadsheet can be found here. However, if you would like to access the template for my finance spreadsheet before reading more about it, click here. To those of you who have joined my journey, thank you again and enjoy the gift in your inbox!

Fave issue of this blog and totally what i needed right now given a disastrous month of spending!

Have purchased the spreadsheet and hopefully this time next year i can be as smart with money as you <3

Thank you for your purchase Abs it is massively appreciated and I am now glad you are on the saving journey with me – I hope you are making use of the spreadsheet! We will definitely catch up and discuss (point 6)

Your spreadsheet is incredible Jag – honestly cannot believe how brilliant it is for the cost. It definitely makes saving achievable for both beginners and those who regularly save already – it’s a great way to create a goal and then make sure that you stay on track.

Thank you Jay and for inspiring my two alternative layout options! It has worked incredibly well for me and I would encourage others to do the same, whether that is using my template or their own!

This was a great blog that was definitely needed going into the new year. The tips you give are ones that most of us are guilty of ignoring, even though some might seem obvious. I think anyone who reads this can agree that it’s a brilliant way to get you back into the mindset of saving. The finance spreadsheet is also amazing and something I certainly live by. Having to personally input your spending habits into the sheet definitely holds you accountable, to the extent that you’ll be thinking twice about certain expenses!

Bang on Sanjeet – the spreadsheet drives accountability and that’s why it is so needed! It can be longwinded at first but if you update it every couple/few days it really is incredible. I am glad I started in 2018 and I am glad you are joining me in tracking – good luck saving!

Someone recently informed me of a quote I’d like to share with you:

“Do not save what is left after spending, but spend what is left after saving” – Warren Buffett

I hope this helps!